An effective way to save tax, as advised by tax consultants, is to form a Hindu Undivided Family. The principle of taxation of Hindu Undivided Family is based on the concept of joint family in India, where the assets are owned jointly by the family, and incomes from such assets are joint incomes for the family. Such joint family incomes cannot be assessed for taxation for a specific individual and is therefore taxed for the whole joint family. What is a Hindu Undivided Family, from an income tax standpoint? A Hindu Undivided Family is a separate legal tax entity under the provisions of S.2 (31) of the Income Tax Act 1961. Members within the Hindu Undivided Family (HUF), who have individual incomes, are taxed separately. For example, if you are in a job and also have rental income from an ancestral property owned jointly by your family as HUF, then your salary will be taxed in your hands while the rental income from your property will be taxed in the hands of the your family (HUF). If you are in a tax slab which is higher than that of your HUF, then you will be able to save tax in such a situation. In this article, we will discuss with the help of an example, how you will be able to save taxes, by forming an HUF.

Who can form an HUF?

- If you are married, you can form an HUF. Apart from Hindus, even Jains, Buddhists and Sikhs can form HUFs, if they are married

- You only need to be married. It is not mandatory to have children to form an HUF

- The eldest male member of the family is the "Karta" of the HUF. The Karta needs to manage the affairs of the HUF and file income tax returns for the HUF

Who can be part of HUF?

- Your children (both sons and daughters), your grand children (both grandsons and granddaughters) and your great grand children (both great grandson and great granddaughters) can be part of your HUF. Your daughter's children will also be part of your HUF. The lineal descendants of the Karta are the co-parcenors in the Karta's HUF. They have equal right over the property of HUF and can demand the partition of HUF

- The parents, brothers, sisters and relatives of the Karta or his wife, cannot be part of HUF. Only the children of the Karta and their children can be part of the HUF

- After the death of the Karta, his eldest son will become the Karta. There is a misconception that only male children can carry on the HUF. If the Karta does not have any male children his wife and daughters can carry on the HUF

- Married daughters can continue to be part of their father's HUF. They can be, at the same time, members of their husbands HUF

- Sons can start their own HUF after their marriage, while being a member of their father's HUF at the same time

How to start an HUF?

- You need to apply for a PAN card for your HUF

- You need to open a bank account for your HUF. The Karta is the authorized signatory for the bank account

- You need to transfer assets to your HUF. Please note that, you can transfer only ancestral or gifted assets to your HUF. This is easier said than done. Property received by way of will, in favour of the HUF, can be transferred to the HUF. However, if the property is bequeathed to you as an individual, you cannot transfer the property to your HUF. You can also transfer gifts received from someone outside your HUF to your HUF. Gifts received during wedding, whether cash or gold, can be transferred to your HUF.

- Avoid contributing your own money, by way of gifts, to your HUF. In that situation the income arising to the HUF will be clubbed with your income and taxed as such.

- However, if you contribute your own money to your HUF and invest it in tax free schemes like life insurance policies, tax free bonds etc, the income arising from such investments will be tax free and can be re-invested in other assets to earn higher income. Such income, even if it is taxable, will be taxed only in the hand of the HUF. Income out of income is outside the provision of clubbing of incomes, as per Income Tax Act.

How can you save tax with HUF?

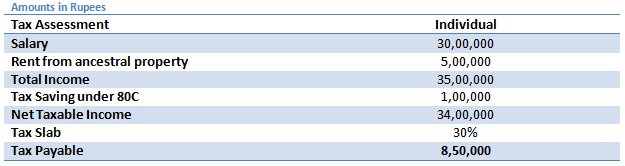

Let us illustrate with the help of an example. Let us assume you are a Hindu married salaried individual and you own an ancestral property. Your salary is Rs 30 lakhs per annum and you get a rental income of Rs 5 lakhs per annum from your ancestral property. Let us assess your total income tax payable in two scenarios:-

- You own the property as an individual

- Your Hindu Undivided Family owns the ancestral property

Scenario 1: You own the property as an individual (i.e. the property is in your name)

Scenario 2: Your HUF owns the property (i.e. the property is in the name of your HUF)

Therefore, in the example above, you can save Rs 1.2 lakhs in tax per annum, if your ancestral property is owned by your HUF. Why is there a difference in the tax liability? It is because the individual and the HUF are treated as two separate tax entities. If you own the property, then the income from the property will be taxed, as per your income tax slab. However, if your HUF owns the property, then it will be taxed at the income tax slab of the HUF. Since the HUF's income falls in a lower tax slab in this example, the tax rate is much lower. Further, your HUF also qualifies for separate 80C deductions. The 80C deduction for your HUF is separate from the 80C deduction that you can claim as an individual. So, if your HUF is able to make 80C investments like life insurance premiums, PPF etc, then your tax liability is even lower. You can contribute to tax free investments under section 80C for your HUF (as discussed earlier).

Conclusion

We have seen in this article, how setting up a Hindu Undivided Family, you can reduce your tax liability arising out of income from assets inherited by you. You should discuss with your chartered accountant or tax consultant, if setting up a Hindu Undivided Family is beneficial for you from a tax perspective. We will discuss other aspects of Hindu Undivided Family tax and financial issues, in future articles in our tax series.

Top 10 Tax Saving Mutual Funds to invest in India for 2016

Best 10 ELSS Mutual Funds in india for 2016

1. BNP Paribas Long Term Equity Fund

2. Axis Tax Saver Fund

3. Franklin India TaxShield

4. ICICI Prudential Long Term Equity Fund

5. IDFC Tax Advantage (ELSS) Fund

6. Birla Sun Life Tax Relief 96

7. DSP BlackRock Tax Saver Fund

8. Reliance Tax Saver (ELSS) Fund

9. Religare Tax Plan

10. Birla Sun Life Tax Plan

Invest in Best Performing 2016 Tax Saver Mutual Funds Online

For further information contact Prajna Capital on 94 8300 8300 by leaving a missed call

---------------------------------------------

Leave your comment with mail ID and we will answer them

OR

You can write to us at

PrajnaCapital [at] Gmail [dot] Com

OR

Leave a missed Call on 94 8300 8300

-----------------------------------------------

No comments:

Post a Comment